Not all things that go up must come down.

Temporarily-Permanent Changes to Tax Law

As a financial planner, I try to find narratives in the tax code to help my clients make use of what is otherwise boring and overly complicated. Back in 2003, George W. Bush signed the Jobs Growth and Tax Relief Reconciliation Act (JGTRRA) and changed the treatment of capital gains taxation in relation to other income.¹ It also lowered the tax rate on capital gains.² Additionally, the JGTRRA made way for a tax bracket with a 0 percent long-term capital gains rate, though it would not take effect until 2008.

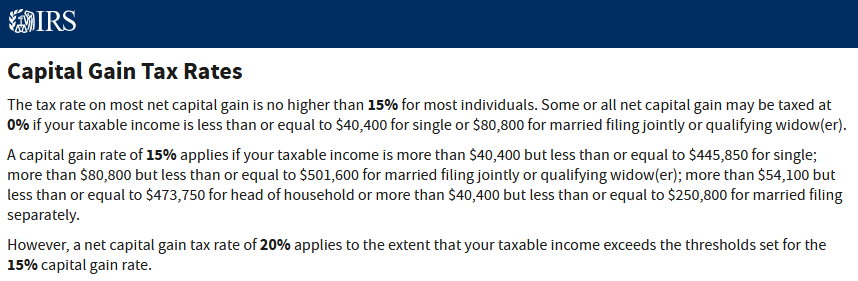

Even though capital gains has a history of preferential tax rates, the JGTRRA was initially proposed as a short-term boost to the US economy after an early-2000s recession. Despite its temporary beginnings, this tax break is still here today. You can find it described on the IRS site if you don’t believe me, excerpted below.

Making Use of the 0% Long-Term Capital Gains Brackets

Like when following a recipe, the order and ratio of ingredients will impact the final outcomes. The examples below are real-life client profiles where we have used the 0 percent long-term capital gains brackets.

Work Transitions

We are often asked where to invest extra income after making IRA contributions. Our answer is to invest in a brokerage account with stocks and mutual funds. These assets are eligible for long-term capital gains rates if they are held for at least one year and a day.

Consider a single-filing individual who has worked for only part of the year. This could be due to entering the workforce after graduation or an early-calendar-year retirement. In this example, the individual has some investment in technology stocks.

For single filers in 2021, the bracket for 0 percent tax on long-term capital gains spans incomes from $0 to $40,400. If the taxpayer earned $15,000 for their partial year of work on top of $30,000 of long-term capital gains in their technology stocks, we would expect them to owe close to $250 in federal income taxes.

- You read that correctly, that’s $45,000 of income with only $250 due in taxes, or a 0.5555 percent effective tax rate.

Supplemental Income while Working

If we consider another case, a married couple that has one working spouse and investments in stocks, bonds, and real estate, they too will have the opportunity to use the long-term capital gains brackets to bring in supplemental income at 0 percent tax.

The 0 percent long-term capital gains bracket spans $0 to $80,800 for a married couple. Let’s assume that the household income from wages is higher than the last case, $60,000 per year. If we add in the same $30,000 of capital gains, the household income is $90,000 and the expected federal tax liability is $3,793 (a 4.2144 percent effective tax rate).

- Put another way: the federal taxes owed at $60,000 of wages is the same as the federal taxes owed in this scenario with $90,000!

Year after year we can help this client capture additional income on their tax return and pay nothing in federal income taxes. This can be used as part of a tax-gain harvesting plan to ensure that you have high-basis stock available for cash flow in your retirement years.

Building a Retirement Bridge until Social Security

For those clients who are ready to retire and are considering how to pay themselves in retirement, we often recommend delaying Social Security and substituting capital gains up to the top of the 0 percent long-term capital gains bracket, whether as a single filing individual or as a couple filing jointly.

Delaying Social Security is a guaranteed increase in eventual benefits received per month – every month of delay adds a credit of ⅔ of 1 percent, which is an 8 percent improvement per year. These credits are earned for those who delay Social Security past full retirement age, but it’s true as well in essence for those that are under full retirement age because of the penalties applied when collecting early retirement benefits.

Consider a couple who have $25,900 of qualified dividends, and $80,000 of long-term capital gains. Unlike our other examples, this couple has no working income but $105,900 of gross income. After the federal standard deduction for a married couple ($25,900), this couple’s taxable income is $80,000.

- In this example, the couple pays $0.00 for federal income taxes.

That’s right, by maximizing the use of qualified dividends and keeping their total taxable income at or below $80,800 this couple pays nothing to the IRS!

Inflation Makes Tax Brackets Bigger

The big takeaway from these examples is easier to see visually. We charted out the effective tax rate for the couple building a bridge to Social Security in our financial planning software, resulting in the graph below. Prior to their retirement at age sixty-one, there was employment income, and as you can see, they had FICA taxes and a marginal tax bracket above 30 percent. At retirement there is a drop in income bringing the couple down to the lowest tax brackets, and this is where the opportunity arises to capture long-term capital gains at 0 percent.

What is especially important to consider is this scenario in the context of history. Today, in 2022, we are experiencing some of the highest inflation in the past four decades. Though the long-term capital gains tax brackets are indexed for inflation, the inflation rate we’re experiencing today is much higher than the time period of 2008 to now. From 2008 to 2022, tax brackets grew at a rate of 1.78 percent; the expected inflation adjustment for the 2023 tax bracket looks to be at least 7 percent!³

As you can see in the graph above from FRED⁴, the inflation we’re experiencing now is not outside of historical bounds but will undoubtedly change the tax brackets more than they have changed since the 0 percent long-term capital gains rate took effect.

Without a doubt inflation is one of the larger risks a retiree faces. Over a time horizon of decades, higher inflation can eat away meaningful chunks of an income. Understanding the tax laws and how you can maximize the return on your investments by capturing a tax-free return can improve a plan’s success rate and longevity. Work with us, your tax professionals, and your budget to stretch out every extra dollar you can.

Doug “Buddy” Amis, CFP®

2. https://www.investopedia.com/terms/j/jgtrra.asp

4. Federal Reserve Economic Data from the Federal Reserve Bank of St. Louis, one of twelve banks of the Federal Reserve System