…and attempts to read the horoscope of Congress

Sunrises and Sunsets

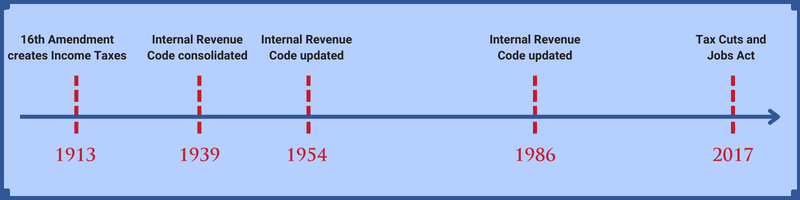

Given how infrequently large tax acts are passed, the Tax Cut and Jobs Act (TCJA) may feel like a once-in-a-generation piece of tax legislation, but know that it is filled with tax ghouls from the past coming back to haunt you. For those who don’t remember, the TCJA was passed and signed into law late in December of 2017 after many late-night negotiations over what would be included or excluded. Necessary to the mechanics (and politics) of passing the bill, Congress made most of the changes for individual taxpayers only temporary.

You may have heard about the provisions of the tax code that “sunset” at the end of 2025 – that’s a nice way of saying these individual tax cuts will expire automatically unless there is congressional intervention to extend them. The “sunset provisions” of the TCJA create limited-time opportunities, and like the moon in the middle of this December, they are waning.

With what made it into the final text of the bill, these are some of the bigger items facing a reset to look out for if you are preparing for retirement or are recently retired:

- Marginal income tax brackets reset to higher brackets from 2017

- Standard deductions drop

- Changes to gifting strategies (both charitable and family)

Rising Marginal Rates

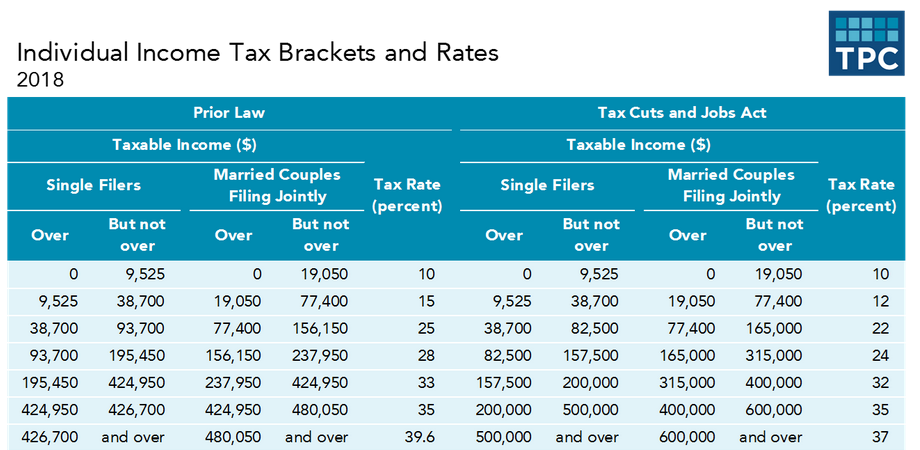

Tax brackets have two components: a marginal percentage tax rate and an income range. With the upcoming reset, we will see most taxpayers paying more. As you can see in the graphic below from the Tax Policy Center, increases in the “Tax Rate” are as little as 3 per cent (32 percent bracket becomes the 33 percent bracket) or as much as 25 per cent (12 percent bracket becomes the 15 percent bracket).

Be on the lookout for opportunities to bring taxable income forward and pay at lower rates. This can be a strategy that is useful for retirees and even pre-retirees that have some “room” left in their tax bracket. For example, a couple with a taxable income of $50,000 may plan to convert $20,000 of pre-tax assets to Roth assets each year prior to 2026. This amount keeps them in their current tax bracket and allows them to squeeze out maximum income at the 12 percent marginal tax rate instead of being taxed at 15 percent after the reset, plus future earnings on the conversion may be accessed tax free.

Two Plus Two Equals Five?

Next we have the sunsetting of the doubled standard deduction and the return of personal exemptions (amounts you can deduct from your adjusted gross income, for yourself and each dependent), which were done away with while the standard deduction was doubled. What does this all mean? For families that have fewer than three children, tax time proved simpler and less expensive with the TCJA changes. Going back to the original tax law, the one with standard deductions and personal exemptions, larger families should benefit while some smaller households may feel squeezed. Unfortunately, a family of any size should prepare for changes that could feel like deja vu.

For example, itemized deductions will again play a larger role in tax planning. During the TCJA many itemized deductions were suspended and the larger standard deduction led to fewer taxpayers itemizing in general. The return of the prior methods will require more in-depth conversations around tracking deductible expenses and specialized income planning to avoid limitations on deductions for high earners (sometimes referred to as the Pease limitations). Many taxpayers in higher-tax states or those who have mortgages will see deductions potentially increase as the $10,000 cap for state and local taxes will go away during the transition into 2026.

Work with our advisors to forecast your personal tax liabilities before and after the sunset to see if it is actually a full moon requiring more attention. Because there are multiple variables involved like the marginal tax, income ranges, and deductions, it is important to know how these numbers really add up instead of making rough estimates.

Higher-income and high-net-worth families should keep reading to see how the reset for estate tax laws and gifting could affect their tax returns and financial plans. The gifting changes will affect gifts to charity and gifts to family.

Mr. Scrooge Returns After December of 2025

Following the TCJA and subsequent Coronavirus-related legislation, higher-net-worth families could benefit more from their charitable gifts. The amount of individual charitable giving may be larger than you expect – in 2021 individuals gave $326.87 billion to charities (representing 67 percent of total giving). But with the TCJA sunset, deductibility for charitable gifts of cash will reset to 50 percent of adjusted gross income (AGI). Charities that grew and expanded during the past two years could find funding drying up.

Should you feel inclined to give to family instead of charity, get the gifts completed before the sunset of the larger unified tax credit. This credit currently allows gifting of $12,060,000 per giftor. Prior to the TCJA, the unified tax credit was half as much, and without intervention by Congress or a change in legislation (like in 2010 when the estate tax was effectively repealed) it will reset to the smaller size. That means the opportunity to make tax-free, life-changing gifts to family or friends is half as large come January of 2026.

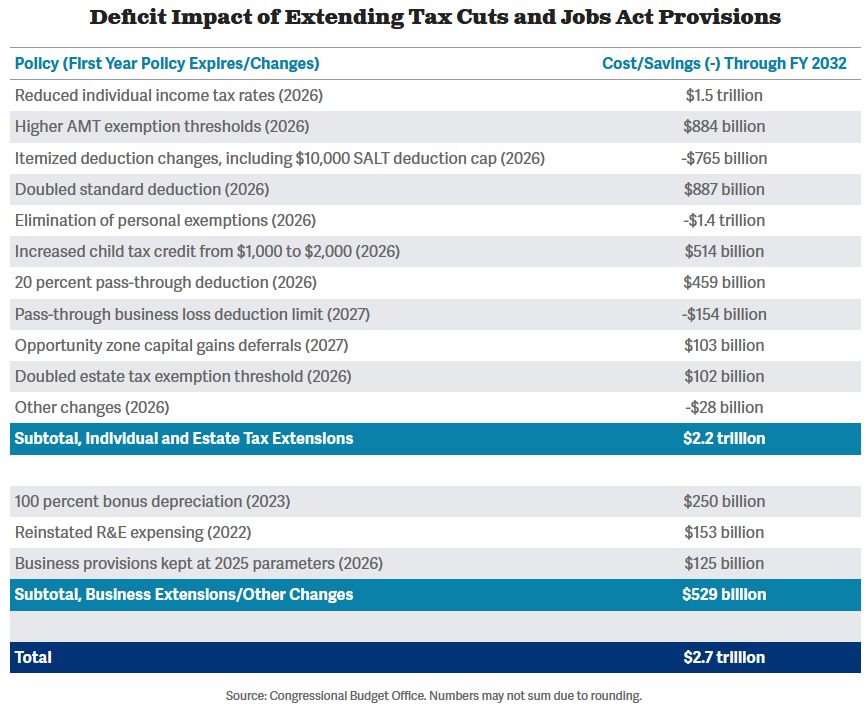

Regardless of the size of your portfolio, the future is uncertain. All of our financial forecasts are subject to more than seasonal changes and phases of the moon – they are subject to Congress, and politicians can choose to ignore the laws of physics. Even calling a tax cut temporary does not mean it will be: temporary tax provisions have become permanent before, like the Bush tax cuts that created the 0 percent long-term capital gains rate we help clients use. The image below shows the Congressional Budget Office’s estimates of the projected costs of extending the temporary provisions over the next ten years. These changes are not cheap and there is no way to perfectly navigate the changing tides of tax law as they ebb and flow under the effects of the sun, moon, and Congress.

No matter what werewolves or politicians are out there, the key to creating a sound retirement income plan that is tax-efficient is flexibility. Contact our team today to review your portfolio and see how tax law could impact your future.

Doug “Buddy” Amis, CFP®